Backdoor Roth Ira Conversion Rules

Over The Roth Ira Income Limit Consider A Backdoor Ticker Tape

Opportunity For High Income Earners The Backdoor Roth Conversion The Astute Angle

Roll Overs Horse Races And Backdoor Roth Ira Strategy S

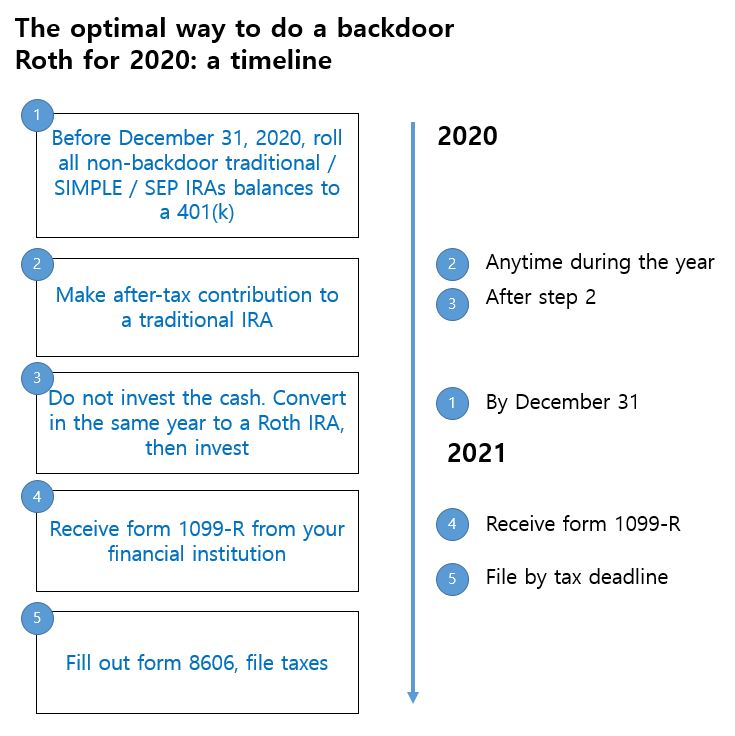

Backdoor Roth Ira Tutorial 2020

The Optometrist S Guide To Roth Ira Chapter 1 Introduction And Backdoor Roth Ira Ods On Finance

Mega Backdoor Roth Convert Within Plan Or Out To Roth Ira

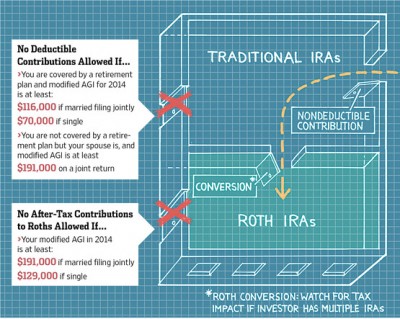

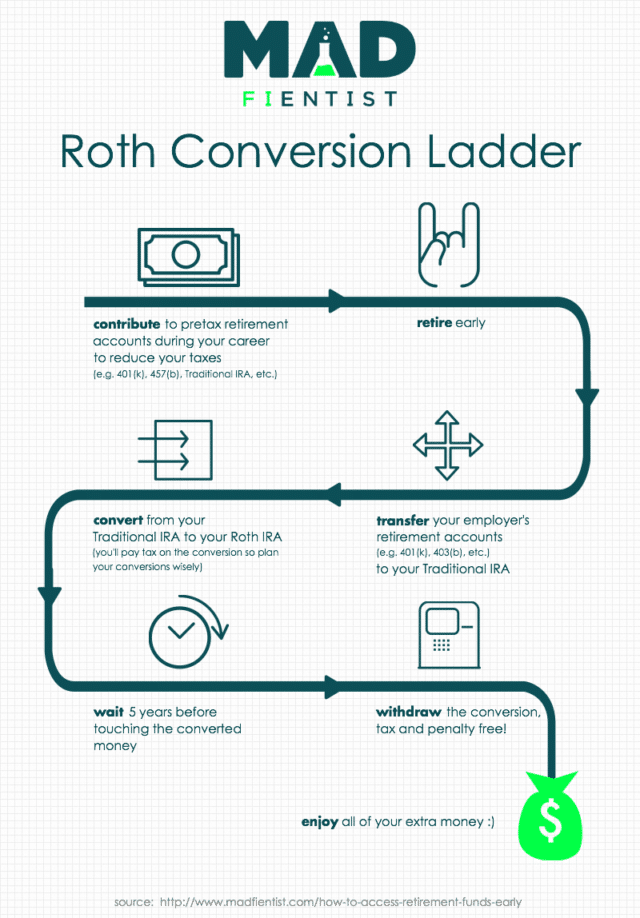

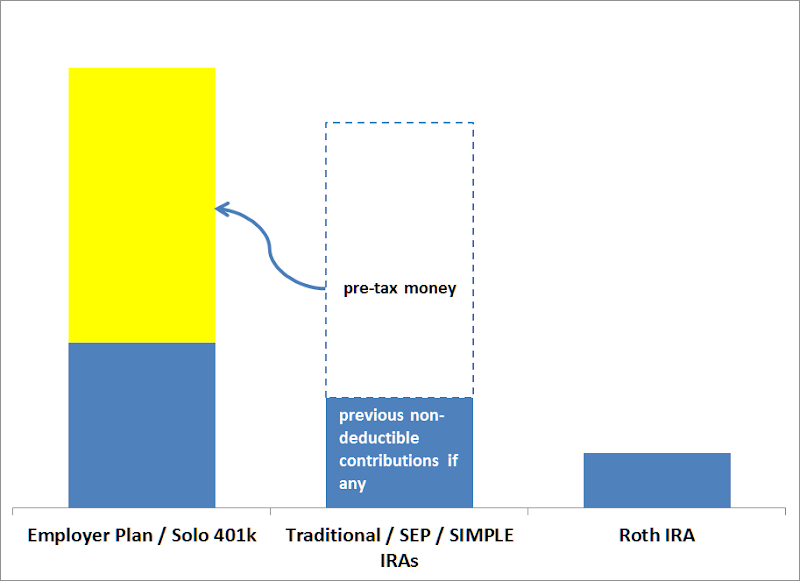

A backdoor roth ira is a legal way to get.

Backdoor roth ira conversion rules.

Backdoor Roth A Complete How To

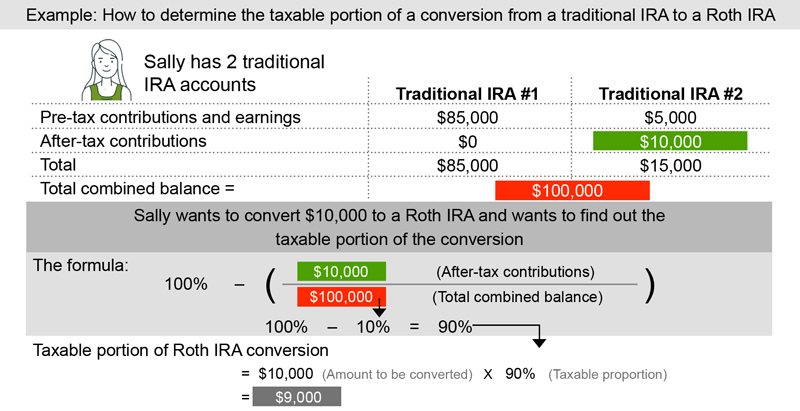

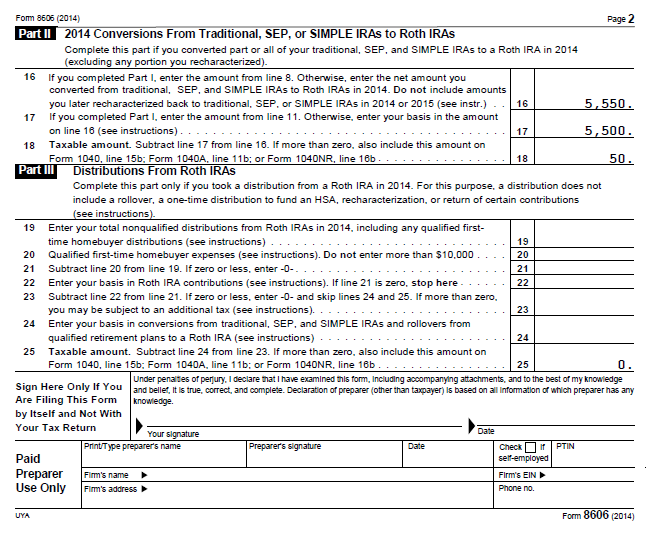

Roth Conversion Q A Fidelity

How To Open A Backdoor Roth Ira

5 Essential Backdoor Roth Ira Facts That You Need To Know Tony Florida

Backdoor Roth Ira Steps Roth Ira Ira Ira Contribution

Fire Did We Screw Up Our Backdoor Roth Save My Cents

The Backdoor Roth Ira Conversion Dental Cpa Dental Consulting Dentist Taxes

Roth Ira Contribution Limits And Using The Backdoor Conversion

Minimize Taxes On A Roth Ira Conversion Betterment

Roth Ira Contributions For High Income Earners Stokes Family Office

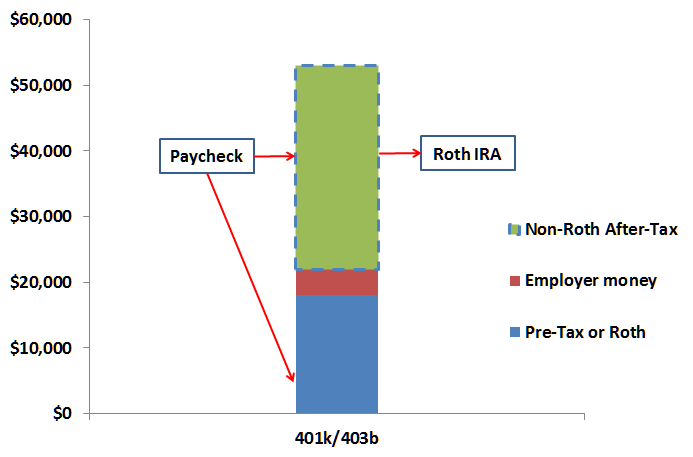

Can I Make A Mega Backdoor Roth Ira Contribution Isc Financial Advisors

How To Do A Backdoor Roth Ira Contribution Safely Ira Contribution Roth Ira Contributions Roth Ira

Why Most Pharmacists Should Do A Backdoor Roth Ira

Yfp 096 How To Do A Backdoor Roth Ira

:max_bytes(150000):strip_icc()/roth-ira-vs-traditional-ira-written-in-the-notepad--1090754116-525e8e6001494031bda19fa01ad1cf2f.jpg)

How To Set Up A Backdoor Roth Ira

What Is A Backdoor Roth Ira Conversion Medicare Life Health

Traditional And Roth Iras Executive Planners Nc

What Is The Backdoor Roth Ira Loophole And Do I Need To Use It

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctqlcayh3c05pzgq0ndk41m51veapl6cbbgfcv9lufs8p7l2iui Usqp Cau

Make Backdoor Roth Easy On Your Tax Return

Backdoor Roth Ira Ultimate Fidelity Step By Step Guide Fatroth

Backdoor Roth Ira How To Convert Personal Capital

Backdoor Roth Ira Conversion Early Retirement Strategy

Backdoor Roth Ira Conversion And Strategy Marketbeat

Source : pinterest.com